South Dakota v. Wayfair: A Brief Update on “Economic Nexus” and How Manufacturers Should Respond

What’s Happened Since the Wayfair Decision?

Back in October, in “What Businesses Need to Know About the Supreme Court’s Wayfair Decision,” we took a look at what was happening in the wake of the Court’s June ruling that economic nexus was, under certain circumstances, enough to allow a state to collect sales tax from a company who had business transactions within that state’s borders, even if the company lacked a physical presence in the state.

At the time, we noted that the ruling had opened the floodgates, allowing states to capture tax revenues that they had long coveted. In the four short months following the decision, “29 states…will be enforcing their new tax authority on Internet sales by January 2019.”

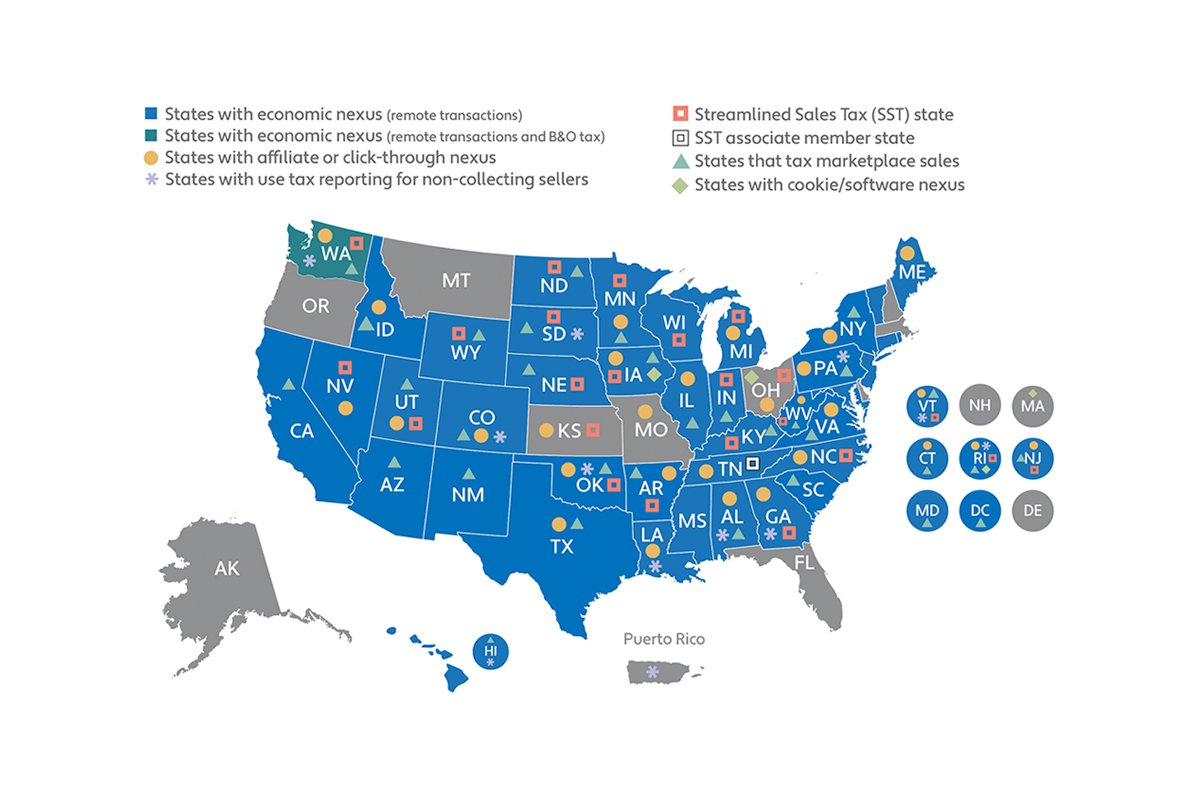

And today? According to Avalara, experts in tax compliance software solutions (full disclosure: Rootstock is a certified solution partner of Avalara), there are now 42 states with a sales tax collection law based on economic nexus (remote transactions).

And while that’s an obvious majority of states, it’s not even the whole picture. As of this writing, only six states – Alaska, Delaware, Florida, New Hampshire, Oregon, and Montana – do not tax remote sales in some fashion. In addition to economic nexus, states are taxing remote sales based on things like ties to in-state affiliates (affiliate nexus), links on in-state websites (click-through nexus), and even if you simply place software or apps on in-state devices (cookie nexus).

What Should Manufacturers Be Doing?

To be honest, how you respond to this new reality will depend on a number of factors. There’s so much state-by-state variance in how taxing authorities have been moving forward with the opportunity to collect sales tax on remote transactions that there isn’t one right answer to the question. But you must answer it. Ignoring this new reality is not an option. If you haven’t already taken aggressive action to understand and address your exposure and obligations, there are two steps we recommend that every manufacturer take now.

First, unless you have the appropriate expertise on staff, engage with an outside firm that has a solid understanding of the landscape and can confidently guide you through the mine field of state-by-state compliance. Even seemingly simple mistakes or oversights could end up costing you a lot of money and time. Besides, who wants to be on the radar of any state-level DOR?

Second, look at options to automate your tax compliance efforts. Trying to deal with this using spreadsheets or other antiquated methods – and yes, that would include accounting software that is not built to deal with the taxation of remote transaction – is asking for trouble.

And know that exempt sellers are not immune to these changes.

Here’s one more caveat: do not sit back and wait for federal legislation to make sense of all this. Congress is showing no appetite (or ability, some might suggest) to bring order out of this chaos. The Remote Transactions Parity Act (H.R. 2193), for example, was introduced in the House on April 27, 2017. It died in committee, and it appears there are currently no bills under consideration. It’s you versus 44 different state taxing authorities.

Wayfair Decision: The Bottom Line

Don’t wait. Even if you’ve executed a state-by-state nexus evaluation since the Wayfair decision, you should implement another one; the situation is that fluid. Engage with your tax advisors to create a plan to track and comply with these new and evolving requirements. You can also find great information and resources at the site of our partner, Avalara, experts in tax compliance software solutions.

Still confused about Sales Tax requirements? You’re not the only one.